HIGH COURT APRIL 2024 WEEKLY ROUNDUP| Stories on Right to sleep, Ayushman Bharat Scheme; Gaurav Bhatia; Dominos Trade Mark; Bigg Boss; and more

A quick legal roundup to cover important stories from all High Courts this week.

Bringing you the Best Analytical Legal News

A quick legal roundup to cover important stories from all High Courts this week.

By Manish Jain†, Ambarish Pandey†† and Shruti Khanna†††

Cite as: 2024 SCC OnLine Blog Exp 15

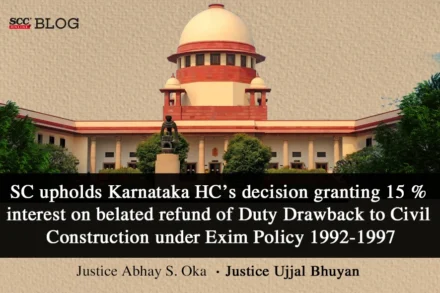

“The benefit of duty drawback would take effect from the date of enforcement of the Exim Policy and in case of belated refund of duty drawback, interest rate fixed by the Central Government at the relevant point of time is applicable”.

Corporate Laws — Company Law — Winding up and Liquidation — Overriding preferential payments: Dues towards customs duty i.e. government dues falling

by Tarun Jain†

Cite as: 2023 SCC OnLine Blog Exp 80

Unless the self-assessed return, as submitted had been questioned, re-opened or re-assessed and the assertion of the petitioner of the services rendered by it qualifying as an “export of service” questioned or negatived in accordance with the procedure prescribed under the Act, its claim for refund could not have been negated.

Latest addition to the landscape of jurisprudence around obscenity laws in India is Saurabh Bindal’s convincing read titled Obscenity: Prevention, Law and

“Provisions in the Customs Act, 1962 do not negate or override the statutory preference in terms of Section 529A of the Companies Act, 2013”.

Importation of gold is a prohibited item within the meaning of Section 2(33) of Customs Act, and that redemption in case of importation of gold that is brought into India illegally in the form of ‘smuggling' does not entitle the owner or importer for automatic release/redemption of such item.

Section 28 provides a window of five years from the relevant date within which proceedings under the said provision may be initiated. The proceedings so initiated are liable to be ended in accordance with the statutory timelines which stand out in sub-section (9).

Bombay High Court expressed that sealing of premises is a drastic action which leads to tinkering with the substantive right to hold, use or occupy immovable property.

by Tarun Jain†

Cite as: 2023 SCC OnLine Blog Exp 28

by Anamika Mishra†

by Nupur Maheshwari†, Harshdeep Khurana†† and Siddhant Indrajit†††

Cite as: 2023 SCC OnLine Blog Exp 2

Detaining Authority gravely erred in relying upon the illegible documents which is equivalent to non-placement of translated-RUDs in a language which the detenu understands, which consequently vitiates the ‘subjective satisfaction’ arrived at by the Detaining Authority.

Tripura High Court: In a public interest litigation seeking issuance of show cause to the respondents as to why a writ of

Nothing could prevent the legislature from specifically incorporating a provision in Section 110-A Customs Act, 1962 to also entitle, besides an owner, an importer, a beneficial owner or any person holding himself to be an importer to claim a right to seek provisional release of goods in terms of Section 110-A of Customs Act, 1962

Supreme Court: The 3-judge bench of NV Ramana*, CJ and JK Maheshwari and Hima Kohli, JJ has held that the Insolvency and

Madras High Court: In a case where show cause notices were sent by Assistant Commissioner of Customs (Respondent 4) for short collection